From Market Trends to the Mortgage Process: Insights for Homebuyers

The last two years have also been complicated for real estate (to say the least). Our Home Buying Survey pooled potential and current homeowners on everything from their future real estate plans to choosing a mortgage in order to understand how we’re feeling right now.

Curious how you stack up?

Most people want to move soon.

The real estate market has been tricky in the last few years (to say the least). First, a surge in buyers pushed housing prices up and limited inventory. Then, rising inflation led to higher mortgage interest rates. But that doesn’t mean you can’t make a move if you want to.

Finding an affordable home is possible in any market but requires research, planning and exploration. Start by establishing a budget. Once you know what you can afford, consider working with a realtor to explore neighborhoods and home types you hadn’t considered before. You could even branch into less explored options like fixer-uppers and foreclosures to broaden your available housing pool.

You can also use our mortgage calculators to help you decide what you can afford and get an idea of what your mortgage might look like.

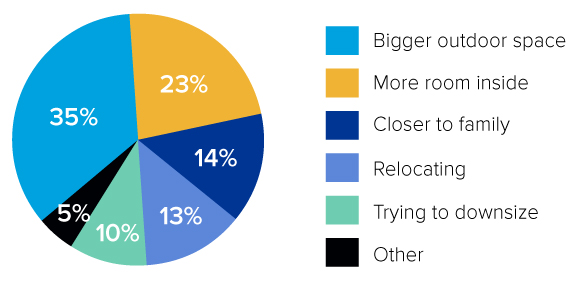

We want more space.

For those planning to move, space is the single driving force. Most people—35%—dream of a bigger outdoor space, while 23% wish their home had more room inside.

Other motivations to move include:

- To be closer to family: 14%

- Relocating: 13%

- Trying to downsize: 10%

- Other: 5%

You may not need to move to turn a good home into a great one. Remodeling can help you plan purposeful spaces that suit your family. Homeowners can utilize a home equity line of credit (HELOC) or a home equity loan to fund their home remodeling projects. Both options allow homeowners to tap into the equity they have built in their homes.

With a HELOC, homeowners can access a revolving line of credit based on the amount of equity they have in their homes. They can borrow funds as needed during a specified draw period, typically around 5 to 10 years. Interest is only charged on the amount borrowed, and homeowners have the flexibility to use the funds for various remodeling expenses. It's important to note that the interest rates on a HELOC are usually variable and can fluctuate over time.

On the other hand, a home equity loan provides a lump sum loan based on the equity in the home. The loan is typically repaid over a fixed term, usually 5 to 20 years, with a fixed interest rate. Homeowners receive the entire loan amount upfront and can use it to finance their remodeling project.

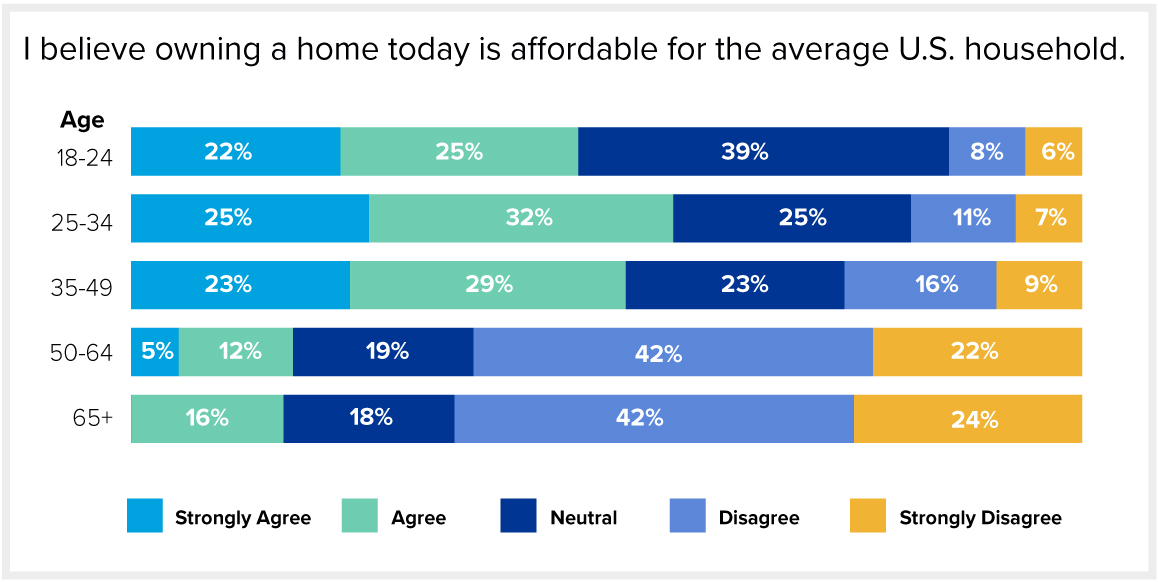

We don’t think homeownership is affordable.

Homeownership may still be the American dream, but many people think that dream is becoming unaffordable. Less than half of those surveyed agreed that homeownership is still affordable for the average household.

Your age range may influence how you perceive affordable housing as well. Overwhelmingly, Baby Boomers think the market has become too expensive, while Gen Z is generally more comfortable with current housing prices.

Who thinks housing isn’t affordable by age range:

- 18 to 24 years old: 14%

- 25 to 34 years old: 18%

- 35 to 49 years old: 25%

- 50 to 64 years old: 64%

First-time buyers often struggle to come up with a down payment, but there are options available.

- FHA loans: The Federal Housing Administration offers loans specifically designed for first-time home buyers with more lenient qualification requirements, lower down payment options and competitive interest rates.

- VA loans: The U.S. Department of Veterans Affairs provides loans to eligible veterans, active-duty service members and surviving spouses. VA loans often offer favorable terms, including zero or low down payment options and competitive interest rates.

- USDA loans: The U.S. Department of Agriculture offers loans for rural and suburban home buyers who meet certain income and location criteria. USDA loans provide low to no down payment options and favorable interest rates.

- State and local first-time home buyer programs: Many areas have their own programs to support first-time home buyers. These programs may offer down payment assistance, closing cost assistance or favorable loan terms.

- Down payment assistance programs: Various organizations and nonprofits provide down payment assistance grants or loans to help first-time home buyers cover a portion of their down payment or closing costs.

You may also find a conventional loan without the standard 20% down payment. Credit unions—like First Tech—offer several programs to help new homeowners get into their dream homes.

Interest rates are still king when it comes to choosing a mortgage.

More than 40% of those surveyed said they opted for the best interest rate they could get, while only 11% went with the referral.

Interest rates can fluctuate daily or even hourly. By locking in a specific interest rate, home buyers gain predictability and safeguard against rate increases during the lock period. Getting pre-approved for a mortgage can lock in your interest rate for a certain period. If interest rates rise after rate locking, you’re shielded from the impact.

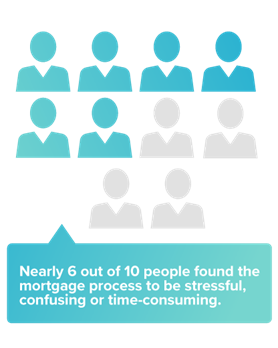

The mortgage process can be confusing.

Nearly 6 out of 10 people found the mortgage process to be stressful, confusing or time-consuming. While only 9% wouldn’t have wanted more guidance on the process.

Nearly 6 out of 10 people found the mortgage process to be stressful, confusing or time-consuming. While only 9% wouldn’t have wanted more guidance on the process. If you’re feeling overwhelmed by the mortgage process, expert guidance is available. Home buyer education courses or workshops are offered by local housing counseling agencies and financial institutions, like First Tech. These courses provide comprehensive information about the mortgage process, including financing options, budgeting, credit scores and documentation requirements.

The mortgage loan officers at First Tech are also happy to help you understand the mortgage and home-buying process and answer any questions you have.

Closing costs can come with sticker shock.

Closing costs can be confusing, especially for first-time home buyers. So it may not come as a shock that 62% of respondents were surprised by closing costs.

62% of respondents

were surprised by closing costs.

Being aware of these costs in advance can help avoid financial surprises at the closing table. Closing costs can vary significantly based on factors such as the property location, purchase price, loan type and lender requirements. On average, closing costs typically range from 2% to 5% of the home's purchase price, but you can request a loan estimate from the lender so you know what to expect. Some closing costs may also be negotiable between the buyer and the seller. It's worth discussing with your real estate agent or attorney to determine if any expenses can be shared or covered by the seller as part of the negotiation process.

We largely understand the financial cost of homeownership.

But largely, we know what to expect. Only 11% of our survey respondents felt they didn’t know what to expect when it came to homeownership costs.

By understanding and budgeting for homeownership costs such as maintenance, insurance, HOA dues, property taxes, utilities and home warranties, homeowners can be better prepared financially and avoid unexpected financial strains. If you find a home you love but aren’t sure of what to expect, work with your real estate agent. They can help you determine what ongoing costs you may have.

Making timely mortgage payments can be a challenge.

When asked if they’d paid their mortgage on time every month, 25% of survey respondents said they’d made at least one late payment in the last four years.

When asked if they’d paid their mortgage on time every month, 25% of survey respondents said they’d made at least one late payment in the last four years.

Despite our best intentions, life happens. Shifts in the economy, worries about a recession on the way and rising inflation have had an impact on many people.

Paying your mortgage on time is crucial for several reasons:

- Credit score: Your payment history significantly impacts your credit score. Late or missed mortgage payments can have a negative effect on your creditworthiness and lower your credit score.

- Avoiding late payment fees: Late mortgage payments often incur penalties or late payment fees imposed by the lender.

- Foreclosure risk: Consistently late or missed mortgage payments can lead to foreclosure. Foreclosure can have severe consequences, including the loss of your home and significant damage to your creditworthiness.

Some moves—like setting up automatic payments or reminders and creating a budget that includes your mortgage payment—can help ensure you make your mortgage payment by the due date. However, if you are having trouble making payments, reach out to your lender as soon as possible. Your lender may be able to help you get over the slump and stay in your home.

Considering buying a home? Your local home loan experts at First Tech are here for you every step of the way—from answering questions to helping with pre-approvals to getting you into your dream home. Schedule an appointment today.

About the survey.

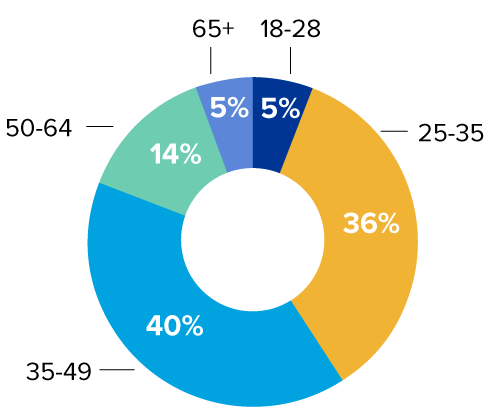

The findings of our Home Buying Survey are based on an online survey of about 800 consumers in the U.S. Participants who had not purchased a home were excluded from the survey. Conducted in June 2023, participants ranged in age from 18 to 85 years old. Around 35% of survey participants identified as male and 65% female.

Respondents by age

18-24: 5%

25-34: 36%

35-49: 40%

50-64: 14%

65+: 5%

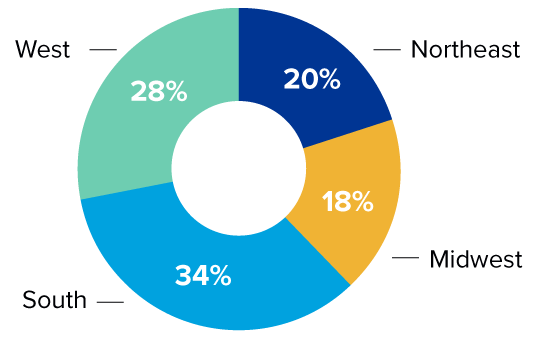

Respondents by geographic region of U.S.

Northeast: 20%

Midwest: 18%

South: 34%

West: 28%

Respondents by age

Respondents by

geographic region of U.S.